At Ridgeline Wealth Advisors, we believe financial literacy should feel practical, not intimidating. Here are four common questions we hear, with straightforward answers to help you think clearly about cash, investing, and market headlines.

Is investing in gold or other metals worth it?

Maybe for some people as a small, specialized part of a broader plan—but not as a guaranteed shield against inflation or market stress. Gold has had significant price swings and has not reliably tracked inflation over long periods. If someone is focused specifically on inflation protection, Treasury Inflation-Protected Securities, or TIPS, have historically been a more direct inflation-linked tool, though no approach is perfect.

Possible benefits of precious metals can include:

- Diversification in some environments

- A tangible asset some people find psychologically reassuring

- Potential value during certain inflationary or crisis periods

But there are also tradeoffs:

- Prices can be volatile

- Gold is not an investment…there are no future expected cash flows so no way to discount cash flow to determine a fair present value share price. It is pure speculation.

- Metals generally do not pay interest or dividends

- Physical ownership can involve storage, insurance, and transaction costs

- Tax treatment can differ from stocks and mutual funds

At a high level, physical gold and many precious metals are generally taxed when sold. Some structures may be treated as collectibles, which can mean different tax treatment than stocks. Some gold ETFs may also be taxed differently depending on how they hold the metal. In some states, sales tax may apply when buying physical metals.

In short, precious metals may have a role for some investors, but they are not a one-size-fits-all solution.

What does it really mean when the stock market drops, and when should we worry?

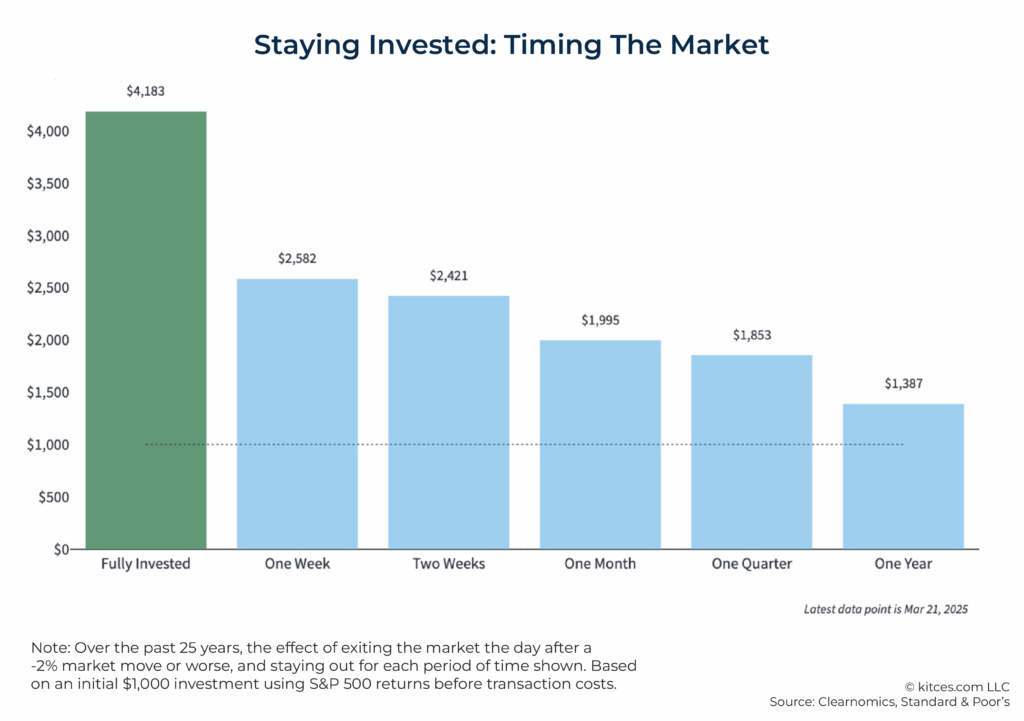

A market drop usually means investors are willing to pay less for many publicly traded companies than they were willing to pay before. That can feel unsettling, but downturns are a normal part of investing and the ‘price of admission’ to get higher expected returns in the long-term. Short-term volatility by itself is usually not a reason to abandon a long-term plan. The better question is often not, “What is the headline today?” but, “Have my own needs changed?”

The S&P 500 is a widely followed index of 500 large U.S. companies, so it is often used as a quick snapshot of how large U.S. stocks are doing. But indexes are not available for direct investment and do not reflect actual portfolio expenses.

Market declines can be uncomfortable, but they are also part of how long-term investing works. For many people, the more important issue is whether their own liquidity needs, time horizon, or risk tolerance have changed—not whether markets are simply having a difficult week.

Is it ever okay to keep cash in a shoebox or under your mattress?

A small amount of physical cash for convenience is a personal choice. But for reserve cash, source materials support prioritizing liquid, interest-earning, FDIC-eligible options over storing large amounts at home. An emergency fund, or protective reserve, exists to help cover unexpected expenses and near-term spending needs without forcing you to sell long-term investments at the wrong time. The exact amount depends on your situation, but the core idea is simple: keep enough cash accessible for real-life surprises.

There is also a tax angle. Money in a savings account may earn taxable interest. Cash at home does not generate taxable interest because it earns nothing. But that comes with tradeoffs: cash at home is easier to lose, steal, or destroy, and it can be harder to document.

How does a CD work?

A certificate of deposit, or CD, is a bank savings product. You agree to leave money at the bank for a set term—such as 3 months, 1 year, or 5 years—and in exchange the bank pays a fixed interest rate. If you take the money out early, the bank will usually charge an early withdrawal penalty. When the CD reaches maturity, you can typically:

- Withdraw the money

- Move it into a new CD

- Let it renew automatically, depending on the bank’s terms

At a high level, CD interest is generally taxable as ordinary income in the year it is credited or made available, even if you do not withdraw it. Banks typically report that interest on Form 1099-INT. Early withdrawal penalties may be deductible on a federal return, and state tax treatment can vary.

Closing Thought

Good financial decisions often start with matching the tool to the goal: cash for short-term needs, savings vehicles for reserves, and long-term investments for long-term objectives. Most financial options are not bad tools to have in the toolbox as long as you know when it’s appropriate to use which tool. Don’t let me find you trying to fix your mirror with a hammer…it won’t go well. Neither will using the incorrect financial tool.