The first three months of the year would not be described as boring by any stretch of the imagination.With the war in Ukraine continuing to create global uncertainty and the government-assisted closing of two of the largest regional banks in history, there is plenty to capture our short-term focus.But even with these and other events, many stock indexes are up since early January and bond prices have seen some recovery as interest rate pressure has eased a bit. The point is that sometimes investment returns can tell a different story than does the current headlines.

However, whether the numbers are up or down in any given year, we caution against letting them alter your mood, or as importantly, your portfolio mix. Because, when it comes to future expected returns, short term performance is among the least significant determinants available.

Thumbs Down…Thumbs Up

In the thumbs-down category, U.S. stock market indexes1 turned in annual lows not seen since 2008, with most of the heaviest big tech stocks2 taking a bath. Bonds fared no better, as the U.S. Federal Reserve raised rates to tamp down inflation. The U.K.’s economic policies3 resulted in Liz Truss becoming its shortest-tenured prime minister ever, while Russia’s invasion of Ukraine and China’s continued COVID woes kept the global economy in a tailspin. Cryptocurrency exchanges like FTX4… well, you know what happened there.

On the plus side, inflation has appeared to be easing slightly, and so far, a recession has yet to materialize. A globally diversified, value-tilted strategy5 has helped protect against some (certainly not all) of the worst returns. An 8.7% Cost-of-Living Adjustment (COLA)6 for Social Security recipients has helped ease some of the spending sting, as should some of the provisions within the newly enacted SECURE 2.0 Act of 2022.

Recency Bias

Now, how much of this did you see coming last January? Given the unique blend of social, political, and economic news that defined the year, it’s unlikely anything but blind luck could have led to accurate expectations at the outset.

In fact, even if you believe you knew we were in for trouble back then, it’s entirely possible you are altering reality, thanks to recency and hindsight bias. The Wall Street Journal’s Jason Zweig7 ran an experiment to demonstrate how our memories can deceive us like that. Last January, he asked readers to send in their market predictions for 2022. Then, toward year-end, he asked them to recall their predictions (without peeking). The conclusion: “[Respondents] remembered being much less bullish than they had been in real time.”

In other words, just after most markets had experienced a banner year of high returns in 2021, many people were predicting more of the same. Then, the reality of a demoralizing year rewrote their memories; they subconsciously overlaid their original optimism with today’s pessimism.

What have we learned?

Where does this leave us? Clearly, there are better ways to prepare for the future than being influenced by current market conditions, and how we’re feeling about them today. Instead, everything we cannot yet know will shape near-term market returns, while everything we’ve learned from decades of disciplined investing should shape our long-range investment plans.

In other words, stay informed but be careful to not be swayed into a reactive decision. Keep your long-term lenses on and your future self will thank you for it.

As we head into a new quarter, always know that we are here to help and are grateful for your continued trust.

Well, we made it to 2021 so how are you feeling? The start of a new year can breed hope for new possibilities. Even though 2020 was oppressive to most in so many ways, I do think we can still hold hope for the new year. I have never been one to focus on New Year’s resolutions as they always felt like a recipe for disappointment (I know that is not the case for everyone, though). What I am striving for this year is not new resolutions, but rather strengthening routines. Routines feel more in my control, and if 2020 taught anything, it is to control what we can control. One of these areas for me is to practice gratitude. I have begun by thinking of 3 things I am grateful for each night before I go to sleep. It is refreshing and encouraging to think on these things. When we talk later this year, feel free to check on my progress with this. This is just one small example, and I am sure that you have others that jump to your mind. Let me encourage you to pursue practices like this for the sake of your own mental health in 2021.

Speaking of control…

You likely have heard us say in the past that market performance is not an area that any of us have control. Because of this, it is wasted energy to focus and worry about market movements. You should spend that energy doing things you can control: spend less than what you make, avoid debt, build cash reserves, plan your generosity and plan your future – practical principals that have an outsized impact on your life.

Small, quiet acts

Whether the temptation is to abandon a free-falling market (like the one we encountered less than a year ago), or chase after winning streaks, an investor’s best move remains the same. Concentrated bets on hot hands generate erratic outcomes, which makes them far closer to being dicey gambles than sturdy investments. Trust instead in the durability of your carefully planned investment portfolio. Focus instead on small, quiet acts. That is what we are here for, for example, to:

– Remind you that your globally diversified portfolio already holds an appropriate allocation to Tesla stock (which may be a lot, a little, or none, depending on your financial goals.

– Guide you in rebalancing your portfolio if recent gains have overexposed it to market risks.

– Help you interpret the 5,600 pages of the newly passed Consolidated Appropriations Act, 2021, so you can manage your next financial moves accordingly.

– Assess potential ramifications of the Biden tax proposals and advise you on any additional defensive tax planning that may be warranted for you in the years ahead.

-Remain by your side as you encounter whatever other challenges and opportunities 2021 has in store for you and your family.

These are not loud acts that you will read about in the paper, but they are the stuff financial dreams are made of. 2021 will be interesting to say the least, but let’s hold onto the hope and possibility that a new year brings. Stay healthy, stay grateful and know that we are here to help.

Josh, Mike, Matt and Sandra

Happy New Year! I hope this message finds you well after enjoying the holidays. I just have a quick note to share to start off our new year. A longer post will be coming later this week as our quarterly letter to clients.

2020 was a tough year on many fronts, but one thing it taught us is that market performance in the short term is wildly unpredictable. In addition, short-term performance will likely have a small impact, if any, on your probability of success with your own financial goals. So it is really not worth your mental energy to ever spend a moment worrying about your short term investment performance. Plus, none of us really have any control over investment performance.

What do we have control over? From a planning and investment standpoint, we discuss fees quite often, and look to reduce this financial headwind where possible because this is something we can control. Most of our clients have Dimensional Funds as core holdings in their portfolio, so we were happy to hear this fall that they announced that fees would be reduced across a broad range of their equity funds effective February 2021, representing an approximate 15% reduction on an asset-weighted basis. They were already significantly lower than the average mutual fund expense ratio, so this is a great move in the right direction. It is exciting because it means that, all else equal, our clients will get to keep more of the investment’s returns which will have a compounding effect on wealth over the years.

Reducing fees is only one way to increase your wealth over time. Let us know if you would like to discuss the other planning tools that can be used to increase wealth as well.

We hope this note finds you well in the midst of turbulent times. We want to recognize the difficulty of the past couple of weeks; in fact, 2020 has been a hard year for almost everyone. As a firm, PLC Wealth is devastated to see the haphazard destruction of life, the mindless assault on personal livelihoods and property, and the highlighted human suffering. We stand with all those on the side of liberty and justice, affirming the American declaration ‘that all men are created equal.’ We hope you all stay safe and healthy in these uncertain times, and as always, please let us know if there is anything that we can do to help.

Most North Carolinian’s are working hard to take care of their families and help their neighbors in the current crisis. Nevertheless, criminals seek to exploit the Covid-19 pandemic to further their scams.

We received the notice below from the North Carolina Secretary of State warning residents to be wary, and we want to share it with you. If you or someone you care about comes across something questionable related to investing or charitable activities, please don’t hesitate to call. We can help you check it out. PLC Wealth is here to help you and answer any questions you have.

Take care, and thank you for your business with PLC Wealth.”

NC Secretary of State Offers Tips to Avoid COVID-19 Related Investment Scams

NC Secretary of State Elaine Marshall is cautioning investors that the ongoing Coronavirus pandemic will likely spark a surge of investment fraud.

“Sadly, scam artists will seek to exploit rising concerns about COVID-19 to draw people into investment traps,” warned Marshall. “Fraudsters often use the day’s headlines in their pitches, so expect to see them prey on the fear surrounding the unfolding Coronavirus pandemic and recent economic developments to promote sham investments.”

The North American Securities Administrators Association (NASAA), of which the NC Secretary of State’s Office is a member, is joining state regulators in offering tips to keep investors safe in these uncertain times.

Bad actors may develop schemes falsely purporting to raise capital for companies manufacturing surgical masks and gowns, producing ventilators, distributing small-molecule drugs and other preventative pharmaceuticals, or manufacturing vaccines and miracle cures.

Scammers also will seek to take advantage of concerns with the volatility in the securities markets to promote “safe” investments with “guaranteed returns” including investments tied to gold, silver and other commodities; oil and gas; and real estate. Investors also can expect to see schemes touting quickly earned guaranteed returns targeting seniors worried about economic disruptions and losses to their retirement portfolios.

“From guarantees of high returns without risk to promises of a miracle cures, if it sounds too good to be true, it probably is,” warned Secretary Marshall. “I urge North Carolinians to follow these tips to help protect your financial and physical health as you navigate these uncertain times.”

Investors are encouraged to call the NC Investor Hotline at (800) 688-4507 or email us at before signing over money in any investment opportunity. If you suspect an investment opportunity is fraudulent, you may report it at www.sosnc.gov. You can also find a wealth of investor education material at www.sosnc.gov/divisions/securities.

Schemes to Watch for:

Private placements and off-market securities. Scammers will take advantage of concerns with the regulated securities market to promote off-market private deals. These schemes pose a threat to retail investors because private securities transactions are not subject to review by federal or state regulators. Retail investors must continue to investigate before they invest in private offerings and independently verify the facts for themselves.

Gold, silver and other commodities. Scammers may also take advantage of the decline in the public securities markets by selling fraudulent investments in gold, silver and other commodities not tied to the stock market. These assets are often promoted as “safe” or “guaranteed” means of hedging against inflation and mitigating systematic risks. However, scammers may conceal hidden fees and mark-ups, and the illiquidity of the assets that may prevent retail investors from selling the assets for fair market value. There are no “can’t miss” opportunities.

Recovery schemes. Retail investors should be wary of buy-low sell-high recovery schemes. For example, scammers will begin promoting investments tied to oil and gas, encouraging investors to purchase working or direct interests now so they can recognize significant gains after the price of oil recovers. Scammers will also begin selling equity at a discount, promising the value of the investments will significantly increase when the markets strengthen. Never lose sight of the risks associated with any prediction of future performance and remember that market gains may not correlate with the profitability of their investments.

Get-rich-quick schemes. Scammers will capitalize on the increased unemployment rate with false promises of quick guaranteed returns that can be used to pay for rent, utilities or other living expenses.

Replacement and swap schemes. Investors should be wary of any unlicensed person encouraging them to liquidate their investments and use the proceeds to invest in more stable, more profitable products. Investors may pay considerable fees when liquidating investments, and the new products often fail to provide the promised stability or profitability. Advisors may need to be registered before promoting these transactions and legally required to disclose hidden fees, mark-ups and other costs.

Real estate schemes. Real estate investments may be appealing because the real estate market has been strong and low interest rates have increased demand. Scammers often promote these schemes as safe and secure, claiming real estate can be sold and the proceeds can be used to cover any losses. However, real estate investments present significant risks, and changes to the economy and the real estate market may negatively impact the performance of these products.

How to Protect Yourself:

The NC Secretary of State’s Securities Division offers this guidance to help investors avoid investment scams:

Ask before you invest. Investors in North Carolina should call the NC Investor Hotline at (800) 688-4507 or email us at to find out if the salesperson and the investment opportunity itself are properly registered. Investors also can check the SEC’s Investment Adviser Public Disclosure database and FINRA’s BrokerCheck. Avoid doing business with anyone who is not properly licensed. If you suspect fraud, please report it to us at www.sosnc.gov.

Don’t get hooked by a phishing scam. Phishing scams may be perpetrated by those claiming an association with the Centers for Disease Control and Prevention, the World Health Organization, or by individuals claiming to offer medical advice or services. Watch out for con artists offering “opportunities” in research and development. These scams may even be perpetrated by people impersonating government personnel, spoofing their email addresses and encouraging victims to click links or open malicious attachments. These emails may look real and sound good, but any unsolicited emails with attachments and web links may be directing you to dangerous websites and malicious attachments that can steal information from your computer, lock it up for ransom, or steal your identity. When in doubt, don’t click.

There are no miracle cures. Scientists and medical professionals have yet to discover a medical breakthrough or develop a vaccine or cure for COVID-19. Don’t fall for online pharmacies claiming to offer vaccines and don’t send money to anyone claiming they can prevent COVID-19, through a vaccine or other preventive medicine.

Avoid fraudulent charity schemes. White-collar criminals may pose as charities soliciting money for those affected by COVID-19. Fake charities will frequently use sound alike names that mimic established charities. Rather than clicking on the links or responding to the email addresses or phone numbers provided in a text, email or social media post, do an internet search to find the charity’s website and reach out to them directly. A link in an unsolicited email could send you to an impostor site. Give generously but wisely to make sure your help is going to those who need it.

Be wary of schemes tied to government assistance or economic relief.The federal government may send checks to the public as part of an economic stimulus effort. It will not, however, require the prepayment of fees, taxes on the income, the advance payment of a processing fee or any other type of charge. Anyone who demands prepayment will almost certainly steal your money. And don’t give out or verify any personal information. Government officials already have your information. No federal or state government agency will call you and ask for personal

There is a good chance that you have more unscheduled time these days as almost every state in the union moves to a stay-at-home orders, but have you used this extra time to read the full H.R. 748 Coronavirus Aid, Relief, and Economic Security Act, or CARES Act? If you would rather use this newly found time in other ways, here is a time-saving summary of the CARES Act looking at 9 different provisions that may impact you. This is a longer post than normal, but is formatted so that you can scan through pretty quickly to sections that are more relevant to you. If you have any questions whatsoever, please be in touch!

CARES Act In General

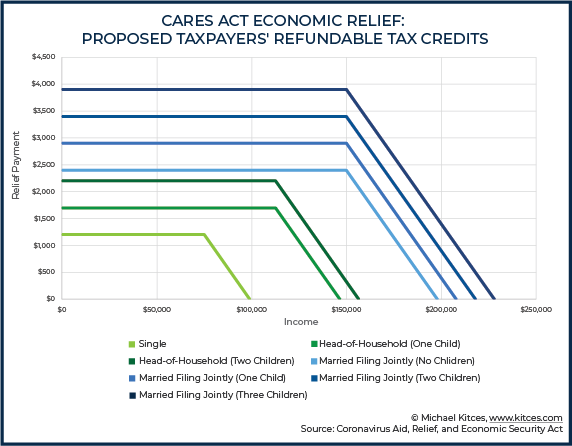

Direct payments/recovery rebates: Most Americans can expect to receive rebates from Uncle Sam. Depending on your household income, expect up to $1,200 per adult and $500 per dependent child. To calculate your payment, the Federal government will look at your 2019 Adjusted Gross Income (AGI) if it’s available, or your 2018 AGI if it’s not. However, you’ll receive an extra 2020 tax credit if your 2020 AGI ends up lower than the figure used to calculate your rebate. This Nerd’s Eye View illustration offers a great overview:

Retirement account distributions for coronavirus-related needs: You can tap into your retirement account ahead of time in 2020 for a coronavirus-related distribution of up to $100,000, without incurring the usual 10% penalty or mandatory 20% Federal withholding. Please note that this is not a waiver of income tax on the distributions, but does allow you to prorate the payment across 3 years. You also can repay distributions to your account within 3 years to avoid paying income taxes, or to claim a refund on taxes paid. There are some landmines here so be careful to follow the rules exactly should you tap in to your 401k.

Various healthcare-related incentives: For example, certain over-the-counter medical expenses previously disallowed under some healthcare plans now qualify for coverage. This also allows for expanded use of tax free money from an HSA. Also, Medicare restrictions have been relaxed for covering telehealth and other services (such as COVID-19 vaccinations, once they’re available). Other details apply.

CARES Act For Retirees (and Retirement Account Beneficiaries)

RMD relief: Required Minimum Distributions (RMDs) are taking a much needed break in 2020 for those meeting the new age requirements, as well as beneficiaries with inherited retirement accounts. If you’ve not yet taken your 2020 RMD, don’t! Let’s talk about other options. If you have taken a distribution, please be in touch quickly with us so that we can explore potential remedies.

CARES Act For Charitable Donors

“Above-the-line” charitable deductions: Deduct up to $300 in 2020 qualified charitable contributions (excluding Donor Advised Funds), even if you are taking a standard deduction. Not much here, but it is worth noting to save a little bit in taxes.

Donate all of your 2020 AGI: You can effectively eliminate 2020 taxes owed, and then some, by donating up to, or beyond your AGI. If you donate more than your AGI, you can carry forward the excess up to 5 years. One big caveat: Donor Advised Fund contributions are excluded.

CARES Act For Business Owners (and Certain Not-for-Profits)

Paycheck Protection Program loans (potentially forgivable): The Small Business Administration (SBA) Paycheck Protection Program (PPP) is making loans available for qualified businesses and not-for-profits (typically under 500 employees), sole proprietors, and independent contractors. Loans for up to 2.5x monthly payroll, up to $10 million, 2-year maturity, interest rate 1%. Payments are deferred and, if certain employment retention and other requirements are met, the loan may be forgiven. The program was set to open up today, April 3, but as of this writing, there is still much up in the air about the actual implementation. If you haven’t already, touch base with your banker as soon as you can.

Economic Injury Disaster Loans (with forgivable advance): In coordination with your state, SBA disaster assistance also offers Economic Injury Disaster Loans (EIDLs) of up to $2 million to qualified small businesses and non-profits, “to help overcome the temporary loss of revenue they are experiencing.” Interest rates are under 4%, with potential repayment terms of up to 30 years. Applicants also are eligible for an advance on the loan of up to $10,000. The advance will not need to be repaid, even if the loan is denied.

Payroll tax credits and deferrals: For qualified businesses who are not taking a loan.

Employee retention credit: An additional employee retention credit (as a payroll tax credit), “equal to 50 percent of the qualified wages with respect to each employee of such employer for such calendar quarter.” Excludes businesses receiving PPP loans, and may exclude those who have taken the EIDL loans.

Net Operating Loss rules relaxed: Carry back 2018–2020 losses up to five years, on up to 100% of taxable income from these same years.

Immediate expensing for qualified improvements: Section 168 of the Internal Revenue Code of 1986 is amended to allow immediate expensing rather than multi-year depreciation.

Dollars set aside for industry-specific relief: Please be in touch for a more detailed discussion if your entity may be eligible for industry-specific relief (e.g., airlines, hospitals and state/local governments).

CARES Act For Employees/Plan Participants

Retirement plan loans and distributions: Maximum amount increased to $100,000 on up to the entire vested amount for coronavirus-related loans. Delay repayment up to a year for loans taken from March 27–year-end 2020. Distributions described above in In General.

Paid sick leave: Paid sick leave benefits for COVID-19 victims are described in the separate, March 18 R. 6201 Families First Coronavirus Response Act, and are above and beyond any benefits received through the CARES Act. Whether in your role as an employer or an employee, we’re happy to discuss the details with you upon request.

CARES Act For Employers/Plan Sponsors

Relief for funding defined benefit plans: Due date for 2020 funding is extended to Jan. 1, 2021. Also, the funding percentage (AFTAP) can be calculated based on your 2019 status.

Relief for facilitating pre-retirement plan distributions and expanded loans: As described above for Employees/Plan Participants, employers “may rely on an employee’s certification that the employee satisfies the conditions” to be eligible for relief. The participant is required to self-certify in writing that they or a direct dependent have been diagnosed, or they have been financially impacted by the pandemic. No additional evidence (such as a doctor’s release) is required.

Potential extension for filing Form 5500: While the Dept. of Labor (DOL) has not yet granted an extension, the CARES Act permits the DOL to postpone this filing deadline.

Exclude student loan pay-down compensation: Through year-end, employers can help employees pay off current educational expenses and/or student loan balances, and exclude up to $5,250 of either kind of payment from their income. If you have a student loan, talk to your employer about this provision. And also pay attention to the For Students section below.

CARES Act For Unemployed/Laid Off Americans

Increased unemployment compensation: Federal funding increases standard unemployment compensation by $600/week, and coverage is extended 13 weeks. If you have lost your job, apply immediately.

Federal funding covers first week of unemployment: The one-week waiting period to start collecting benefits is waived. Again, if you have lost your job, apply immediately.

Pandemic unemployment assistance: Unemployment coverage is extended to self-employed individuals for up to 39 weeks. Plus, the Act offers incentives for states to establish “short-time compensation programs” for semi-employed individuals.

CARES Act For Students

Student loan payments deferred to Sept. 30, 2020: No interest will accrue either. Important: Voluntary payments will continue unless you explicitly pause them. Plus, the deferral period will still count toward any loan forgiveness program you’re in. So, be sure to pause payments if this applies to you, lest you pay on debt that will ultimately be forgiven.

Delinquent debt collection suspended through Sept. 30, 2020: Including wage, tax refund, and other Federal benefit garnishments.

Employer-paid student loan repayments excluded from 2020 income: From the date of the CARES Act enactment through year-end, your employer can pay up to $5,250 toward your student debt or your current education without it counting as taxable income to you.

Pell Grant relief: There are several clauses that ease Pell Grant limits, while not eliminating them. It would be best if we go over these with you in person if they may apply to you.

CARES Act For Estates/Beneficiaries

A break for “non-designated” beneficiaries: 2020 can be ignored when applying the 5-year rule for “non-designated” beneficiaries with inherited retirement accounts. The 5-Year Rule effectively ends up becoming a 6-Year Rule for current non-designated beneficiaries. This is still going to be tricky, so please contact us before taking any further distributions from an inherited retirement account.

Now you are familiar with much of the critical content of the CARES Act! That said, given the complexities involved and unprecedented current conditions, there will undoubtedly be updates, clarifications, additions, system glitches, and other adjustments to these summary points. The results could leave a wide gap between intention and reality. As such, before proceeding, please consult with us and other appropriate professionals, such as your accountant, and/or attorney on any details specific to you. Please don’t hesitate to reach out to us with your questions and comments. We look forward to hearing from you soon!

This will be the quarter that we look back on and never forget. It was the time that a virus spread with a silent vengeance, and the world came to a screeching halt. You may be feeling quite disoriented, fearful or even anxious as you read this note since ‘normal’ for all of us has been shaken to its core due to Covid-19. You are likely hunkering down at home, which is what you should do, with little of your regular activities to keep you busy. If you are like me, it literally feels like the earth has stopped spinning on its axis. Up is down, and right is left. Trust me when I say that it is completely normal to feel this way in the context of what we are dealing with as a human species.

I do not come to you with answers or any conclusions that will change the world…there are people that are much smarter than me working on that now, and I have confidence that they will figure it out. But I can bring some encouragement and suggest some small actions that might, just maybe, help us feel like planet earth is starting to rotate once again.

What can you do?

The spread of Covid-19 has impacted the global economy with a speed and impact that is unlike anything seen in our lifetime. This does not mean that happiness and contentment are totally out of your control, however. Mindset is key…start by realizing that the sun still rises every morning like the picture at the top of the article. There is new hope with each new day. I am sure you have found, as have I, that there is now more time to watch movies, read a book, take a distance-appropriate walk to enjoy the spring weather or call someone (yes, actually call them rather than text) to see how they are doing.

If you are sheltering at home with loved ones, you have probably seen them more in the last two weeks than you have for months. We should all continue to do more of these things, and the more we do, the more connected we will stay. I am not a loquacious extrovert, but I have thoroughly enjoyed being around and talking with the ones I care most about. And the more connected we stay, the more human we will feel. This is where happiness and contentment hide, not in your investment portfolio or the latest round of news.

What are we doing?

Actions taken during times of fear in the markets will have implications for years to come. The question is whether they will be positive or negative. For the long-term investors, which are clients that we serve, volatility creates opportunity. We have taken advantage of this opportunity by tax loss harvesting, which allows us to realize the losses for tax savings, but then invest the proceeds right back in something else so the money is never out of the market. The tax savings for our clients this year will be significant. We have also looked to strategically rebalance portfolios. Because some of the fixed income assets have gains over the last year, we have sold those gains to go buy equity funds that are now at a discount. It rebalances the ship and holds to the strategy of selling high and buying low.

What is next?

The fact is, I don’t know. No one does, but that’s OK. We are still waiting on the details of the massive Stimulus bill that was signed into law on March 27th. There are too many details for me to summarize here. If you want a deep dive in to the details, you can find that here. I plan to write more on this soon, but if you have any questions about this, please do not hesitate to call our office. We are all working remotely, but the extensions still ring right to us. Know that we are here to help in this time of uncertainty. Your well-being is of greatest concern to us, and not just financially. Be safe, be smart, and be part of the global solution for everyone by staying home.

To say the last couple of weeks have been unexpected, unparalleled and dizzying would still be understating exactly what we have lived through in the last few weeks. Based on further news today (specifically, the Stay at Home Orders issued by Wake County, NC for our local clients), most of us will be sheltering in place for the coming weeks, as we should. I have listened intently, as I am sure you have, to all sides of the discussion that has carried on since the beginning of the outbreak. At this point, the experts are making the case for the seriousness of the virus as it spreads exponentially, and that it is likely that the healthy and optimistic among us could be putting our most vulnerable at risk. Slowing down our movement even further, whether by choice or by requirement, seems to be inevitable for a while longer to give us all the best opportunity to get through this. While we do not know how long this Covid-19 virus will last, I want to take a few moments to speak to you directly about what we are doing as a firm and how you can continue to reach us during these times.

We have implemented many changes in the last couple of weeks as part of our Business Continuity Plan due to Covid-19. Thankfully, we were prepared for a remote working environment, and hopefully you have seen no interruption in the normal service from our team. We have all set up our home workspace. This give us access to our email, phone calls, and client files just as easily as we have them in the office. Our phone service is fully digital which means we can take it with us wherever we go. If you call the office and dial my extension, it will ring my mobile phone. If I call you from my mobile phone, I will be doing so from my office line. We also have a fully digital and secure document management system for our firm which means we can safely access all your files at any time of day from any location in the world. Additionally, all our portfolio management, financial planning and client relationship software is cloud-based and accessible from any location. Believe it or not, it really did not take much time for PLC Wealth to convert to a virtual firm with the same capabilities as when physically in the office.

Now, obviously, there are some challenges. It is impossible to fully replace the face-to-face relationship, both for our internal operations and for our client relationships. We are utilizing a secure and compliant messaging tool for internal communications. While there may be times that we need to access the office, we are attempting to have only a 1-person max in the office at any time. We will also plan to continue with client meetings moving forward through virtual meeting technologies such as Zoom. If you do not have access to a computer for such a meeting, we can still have a conversation the old school way…over the phone…in order to make sure that we do not fall behind in our relationship with each of you. Again, if you need us in the meantime, we are an email or phone call away, just as we have always been.

There are a few logistical items to cover: First, mail will be checked regularly, but maybe not every day. Additionally, we have always made the effort to suggest linking your personal bank account to your brokerage accounts to allow for quick money movements back and forth, should they be necessary. Since we are no longer at the office, a time like this makes it necessary. So, if you need to make an IRA contribution or want to add funds to your brokerage account, we can still do that by an electronic transfer. Getting money from your accounts is just as easy, or we can have a check mailed to you. The bottom line is that getting money from your accounts or to your accounts is just as easy as always. Finally, if you have actual stock certificates, those must be mailed directly to TD for deposit in your account, so just let us know if you need the mailing address.

Unfortunately, times of crisis create opportunities for bad actors. There are already stories of scams coming to the surface, so be prepared and know what to look for:

– There are no miracle drugs or remedies for Covid-19 at this time so don’t fall for this one. And do not click on any links that may be in an email stating such things, as the link may be another way to inject a virus on your computer.

– Be very skeptical of any investment ‘opportunities’ with research claims that are no supportable. People will make wild claims to prey on other’s hopes and inability to use the rational brain in times of stress.

– Never, never, never disclose your social security number, account numbers, or any other piece of Personally Identifiable Information (PII). There are rumors that spam calls and emails are already going out claiming that thsi information is needed to get your piece of the Stimulus bill or a tax refund. Hold on to your PII like you (financial) life depends on it.

– Generally, just be skeptical in these times of anything that seems too good to be true. If you are not sure, get in touch with us to talk through it.

Let me leave you with a little encouragement in the midst of Covid-19 . Take this time to do something that many of us no longer do naturally on our own…slow down, exercise (by yourself), rest, re-energize, call someone you haven’t spoken with in a while, or binge watch movies with your family that you never have the time for…but mostly, just look around you to see all of the blessings that you inevitably still enjoy. Sometimes, when we are not able or willing to do that which is in our best interest, it is necessary for it to be forced upon us. We find ourselves in one of those times in history. We are a creative and adaptive species so I look forward to hearing about some of the ways that you will get through this…because you will get through this. I will leave you with three pieces of advice that I am confident will be good for you in the long run…Wash your hands, don’t touch your face, and don’t touch your stocks. Know that we are committed to continuing to serve you and your family. We will strive to provide you with an even higher level of service than that which you have come to expect from us. If you need anything at all, even if it is just to have a conversation about the events of the day, please let us know. We are here to help.

What if Charles Dickens had begun his classic “Tale of Two Cities” as follows: It wasn’t the best of times, it wasn’t the worst of times, it was the usual mixed bag.

While the statement may reflect reality, it doesn’t grab your attention half as well as Dickens’ actual opening sentence describing the French Revolution. As he concluded about the period, “some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.”

Thus, we’ve long known about our infatuation with extremes – Best! Worst! Delight! Despair! These are the sentiments that fuel our dreams and inspire our works of art. But you do yourself a disservice if you allow superlatives to rule your investing. In capital markets, if you get caught up in extremes and devalue the sweeping tides of time, you risk giving up your greatest edge: a clear-eyed understanding of what’s really going on.

As we reflect on the events of 2018, here are two evidence-based points worth repeating:

To quote a more contemporary source than Dickens, Cliff Asness of fund manager AQR recently observed: “This world is pretty much designed to convince us that we’re always at DEFCON 1, when 5 is the mode and 4.5 the mean.”

Other year-end analyses concluded that market volatility for 2018 remained on the low side. Even the wilder swings toward year-end were not that remarkable in the grand scheme of things.

And yet, many “noisiest authorities” have been quick to play up the superlatives, while downplaying how these sorts of best of times, worst of times conditions have long been more the norm than the exception in capital markets. As expressed in this Forbes column, “when you take the long view – and if you’re a long-term investor, then you should – you’ll see that what feels jarring right now is actually just a return to normal levels of short-term volatility.”

This brings us to our second point.

2. You are human; you are susceptible to recency bias.

While there are many behavioral biases that trick us into sabotaging our best financial interests, we’re especially interested in the damage recency bias could cause in current conditions.

Recency bias can trick your brain into downplaying decades of robust market performance data, while magnifying the run of unusually calm market conditions we’ve been enjoying relatively recently – essentially since March 2009. This in turn may lead you to lend more weight than is warranted to current volatility.

That’s not to say the ride will be fun if we encounter more turbulence ahead. But by remembering extremes are actually the norm in your quest to generate durable long-term returns, you stand a much better chance of preserving your objective perspective and your portfolio, come what may.

We are grateful for the opportunity to remain at your side, ever eager to advise your course through whatever the markets have in store for us in 2019 and beyond. How can we help? Let us know!